It's a Money Thing is a collection of effective financial education content designed to engage

and teach young people and adults. Its clever content is delivered in easy to digest quick bites,

making learning about finances interesting and engaging. Each unit features a short video, a

worksheet, an article, and a Power Point presentation. You can pick and choose what you want

to use, and all topics are aligned with the Council for Economic Education's National Standards

for Financial Literacy.

While bank and banking are universally understood and accepted terms, the term

credit union is still largely misunderstood and unknown to many. Credit union is an unusual term,

isn't it? Is it just another name for a bank? Is it a credit card company? Do I have to be in a

union to join?

Think about it: it likely took place before your first job, even as far back

as when your annual income consisted of Tooth Fairy money and lucky pennies. The very first

financial decision you ever made is also one of the most important choices—it's where to keep your

money.

Think about it: it likely took place before your first job, even as far back as

when your annual

income consisted of Tooth Fairy money and lucky pennies. The very first financial decision you

ever made is also one of the most important choices—it's where to keep your money.

Think about it: it likely took place before your first job, even as far back

as when your annual income consisted of Tooth Fairy money and lucky pennies. The very first

financial decision you ever made is also one of the most important choices—it's where to keep your

money.

Supporting your local community is a positive thing—it builds relationships,

it

strengthens the local economy, and it makes your neighborhood a happier and healthier place to

work and play.

Supporting your local community is a positive thing—it builds relationships,

strengthens the local economy, and it makes your neighborhood a happier and healthier place to

work and play.

Credit Union Myths address four common misconceptions surrounding credit

unions. Members will learn how credit unions compare to other financial institutions when it

comes

to service, safety and access to funds.

Credit Union Myths address four common misconceptions surrounding credit

unions. Members will learn how credit unions compare to other financial institutions when it

comes

to service, safety and access to funds.

Asking the right questions is an important part of every financial decision you make, and home

ownership is no exception. If you've been thinking about buying a place, preliminary research will

turn up a long checklist of questions for you to ask at every part of the process. There are

questions for your financial institution, questions for your mortgage broker and questions for

your real estate agent. But what about the questions you should be asking yourself?

Successful scholarship applications take considerable time and effort. Although there's no

shortcut to a quality application, there are steps you can take to make your efforts as rewarding

as possible.

When it comes to buying a new car, you have three options: purchasing it with cash,

purchasing it through a loan (also known as financing) or leasing it. For most shoppers,

the decision comes down to buying or leasing.

The average person moves residences about 11 times in their lifetime. That provides a lot of

opportunity to confront the following question: is it better to own your home or to rent it? It's

a huge decision that affects your lifestyle as much as it does your finances, and the answer will

vary depending on who you ask.

Loans help finance some of our biggest goals in life. They can provide access to possibilities

that we can't afford upfront—possibilities like going to school, buying a home, or starting a

business (to name just a few).

Aspectos básicos de los préstamos

Estos materiales son una buena introducción a los tipos de préstamos y su vocabulario, y se

pueden usar como un repaso antes de abordar temas más avanzados en ese rubro.

If you're considering financing your college education with the help of a

student loan, the

smartest thing you can do for yourself is to only borrow what you truly need. (This advice applies

to pretty much all loan products, by the way.) Pursuing post - secondary education should be an

exciting time in your life. You're making decisions and opening up possibilities that will shape

your future - a future that is adventurous and fulfilling and that decidedly does not include

years and years of crippling debt.

If you're considering financing your college education with the help of a

student loan, the

smartest thing you can do for yourself is to only borrow what you truly need. Learn how here.

Responsible debt repayment is a valuable skill when it comes to borrowing money. Without it,

regular purchases can lead to extreme financial hardship. This lesson introduces students to three

popular debt repayment strategies (the Snowball method, the Avalanche method and Consolidation)

and a personal debt repayment plan.

Estrategias para el pago de la deuda

En estos materiales se describen tres enfoques para diseñar un plan para pagar las deudas: el

método de la bola de nieve, el método de la avalancha y la consolidación.

Like local car dealerships and personal injury law firms, short-term and payday

lenders tend to

have the most irritating commercials on TV. They're often tacky and annoying, and tend to air

during daytime talk shows or very late at night. Their promises of “fast cash!”, “guaranteed

approval!” and "no credit check required!” are enough to make you change the channel—and yet, if

you ever find yourself in a situation where you need to get your hands on some extra money fast,

those commercials might start making sense to you. If your car breaks down or you are short for

this month's rent payment and you have no emergency funds set aside, going to a payday lender or a

pawnbroker may seem like your only options. However, the loans that they offer can be outrageously

expensive and targeted at people who are clearly in a tight spot to begin with, which makes those

businesses prime examples of predatory lending.

If your car breaks down or you are short for this month's rent payment and you have no emergency

funds set aside, going to a payday lender or a pawnbroker may seem like your only options.

However, the loans they offer can be outrageously expensive and targeted at people who are clearly

in a tight spot to begin with, which makes those businesses prime examples of predatory lending.

Walk through the benefits of buying used and

learn what to check for and how

to get the best deal. This will help your young members and potential members make informed

decisions before committing to a such a major purchase.

Walk through the benefits of buying used and

learn what to check for and

how to get the best deal. This will help your young members and potential members make informed

decisions before committing to a such a major purchase.

Paying for school is an important subject that requires a proactive approach,

since so much is left up to the individual student. By understanding student loans, grants, awards

and scholarships, students can get ahead of the game in financing their education.

Paying for school is an important subject that requires a proactive approach.

By understanding student loans, grants, awards and scholarships, students can get ahead of the

game in financing their education.

Living on your own for the first time can be empowering, but bills tend to

sneak up on us because they don't fit nicely into a routine. They all have different due dates;

some are delivered to your mailbox and others to your inbox. Some need to be paid monthly and

others yearly, and some have amounts that fluctuate. It takes a lot of wrangling to get them all

under control. Learn how to make it all work.

Living on your own for the first time can be empowering, but bills tend to

sneak up on us because they don't fit nicely into a routine. They all have different due dates;

some need to be paid monthly, others yearly, and some have amounts that fluctuate. It takes a lot

of wrangling to get them all under control. Learn how to make it all work.

Picture this scenario: you're steering your shopping cart through the sliding

doors of the supermarket, shopping list in hand. As you walk the aisles, there's a strategy you

can use to save an average of 33% on your entire purchase. It doesn't require any coupon cutting

or signing up for rewards cards. And the best part? You still get every single item on your list.

The secret? Buying private-label products instead of brand-name products.

Picture this scenario: you're steering your shopping cart through the sliding

doors of the supermarket, shopping list in hand. As you walk the aisles, there's a strategy you

can use to save an average of 33% on your entire purchase. No coupons or rewards cards needed. And

the best part? You still get every single item on your list.

When you start looking for financial advice (or any kind of advice, for that

matter), experts will share their take on what's “good” and what's “bad.” In personal finance,

there are some classifications that we can all agree on: Debt is bad. Emergency funds are good.

Overdrawing your account is bad. Earning interest on your savings is good. If you're waging an

inner battle of good vs. bad every time you pull out your credit card or take a peek at your bank

statement, it's probably time to give your views on budgeting a shake up.

In personal finance, there are some classifications that we can all agree on:

Debt is bad. Emergency funds are good. Overdrawing your account is bad. Earning interest on your

savings is good. If you're waging an inner battle of good vs. bad every time you pull out your

credit card or take a peek at your bank statement, it's probably time to give your views on

budgeting a shake up.

Learn the basics of effective money management. It's easy to blame our budget

failures on the numbers we use, or the categories we create, or even the specific budgeting system

we choose—but, the underlying cause of a hard-to-stick-to budget is our relationship with it.

These ground rules will set you up for success by changing the ways you look at budgeting.

Learn the basics of effective money management. It's easy to blame our budget

failures on the numbers we use, or the categories we create, or even the specific budgeting system

we choose—but, the underlying cause of a hard-to-stick-to budget is our relationship with it.

These ground rules will set you up for success by changing the ways you look at budgeting.

Aspectos básicos del presupuesto

En estos materiales se presentan algunos conceptos generales que pueden

aplicarse a cualquier sistema de presupuestos, y se resalta que esta actividad debe llevarse a

cabo desde la confianza y no a partir de la culpa.

Budgeting is a skill that helps you make smart decisions with your money. It

ensures that you're spending less than you earn, it prepares you for life's curveballs, and it

funds your goals and your dreams.

Budgeting is a skill that helps you make smart decisions with your money. It

ensures that you're spending less than you earn, it prepares you for life's curveballs, and it

funds your goals and your dreams.

Construir un presupuesto

Estos materiales presentan el popular sistema 50/30/20 para hacer presupuestos.

Los miembros aprenderán cómo establecer su propio presupuesto y catalogar sus gastos como

Necesidades, Deseos y Ahorro.

Checks hold an odd place in our personal finances. In many ways, checks seem

like relics from a previous era. However, despite their gradual decline in use, checks haven't

become completely extinct. We still keep our money in checking accounts, will still balance our

checkbooks, and new banking technologies (Mobile check imaging is one example) are being

introduced to improve the process of paying by check. So, there are still a couple of check

related best practices that you need be aware of to stay on top of your finances.

Despite checks gradual decline in use, they haven't become completely extinct.

We still keep our money in checking accounts, balance our checkbooks, and new banking technologies

(like Mobile check imaging) are being introduced to improve the process of paying by check. So,

there are still a couple of check related best practices that you need be aware of to stay on top

of your finances.

According to the American Pet Products Association, nearly 70% of all US

households own a pet. That translates into an estimated $86 billion spent on food, supplies,

medical care and pet services in 2018. Although the love and companionship our furry (or

feathered, or scaly) friends provide is priceless, it's impossible to ignore the effect that pet

ownership has on our wallet.

Budgeting is a skill that helps you make smart decisions with your money. It

ensures that you're spending less than you earn, it prepares you for life's curveballs, and it

funds your goals and your dreams.

"When I grow up, I want to be a ___." Depending on who you are, filling in the

blank above can be an exciting, troubling, or outright confusing task. If you happen to be a

kindergartner, filling in the blank is awesome, because at that age, dinosaur and superhero are

both perfectly viable career options. If you happen to be in high school, filling in the blank can

be motivating because it takes all your talents and interests and captures them in a single goal

that you can pursue through high school and past graduation day. If you happen to be an adult,

filling in the blank can be a little bit terrifying because that could mean you're now a grown-up

(regardless of whether or not you feel like one) and here you are, still secretly looking for

ideas.

Filling in the blank of who we want to be can be an exciting, troubling, or

outright confusing task. If you happen to be a kindergartner, it's awesome, because at that age,

dinosaur and superhero are both perfectly viable career options. As an adult, filling in the blank

can be a little terrifying because that could mean you're now a grown-up (whether or not you feel

like one) and here you are, still secretly looking for ideas.

Common Money Beliefs are designed to get young adults thinking about the

underlying beliefs that influence their financial decision-making. The handout is a printable

personality quiz that makes for a fun activity either before or after a presentation.

Common Money Beliefs are designed to get young adults thinking about the

underlying beliefs that influence their financial decision-making. The handout is a printable

personality quiz that makes for a fun activity either before or after a presentation.

It's hard to ignore the appeal of making real money online—after all, we

live

in a world where bloggers land book and movie deals, where top YouTubers are multimillionaires

and

where celebrities collect thousands of dollars in exchange for a single sponsored tweet. Learn

strategies for pointing & clicking your way to some extra income.

It's hard to ignore the appeal of making real money online—after all, we

live

in a world where bloggers land book and movie deals, top YouTubers are multimillionaires and

celebrities collect thousands of dollars in exchange for a single sponsored tweet. Learn

strategies for pointing & clicking your way to some extra income.

Choosing a career is tough. Whether you're a new grad or considering a

career

change, it's easy to feel overwhelmed when tasked with selecting your next gig. And why

shouldn't

it? It's an enormously costly decision, in terms of both time and money. In many cases, it

defines

your lifestyle: it determines where you live, how you spend your time and what you can afford.

It

has influence over your stress levels and your general happiness. It's a big deal and, to

complicate matters further, there are over 10,000 options to choose from—even Barbie has had

130

different careers over the years!

Choosing a career is tough. Whether you're a new grad or considering a

career

change, it's easy to feel overwhelmed when tasked with selecting your next gig. It can define

your

lifestyle: determine where you live, how you spend your time and what you can afford. It's a

big

deal because there are many options - even Barbie has had 130 different careers over the

years!

It's the night before the interview. Your outfit is all laid out, your

resumé

is hot off the press and you've Google-Mapped your route. You've done your company research

and

you've practiced answering the tough questions. You are perfectly prepared—and you still feel

like

a nervous wreck.

It's the night before the interview. Your outfit is all laid out, your

resumé

is hot off the press and you've Google-Mapped your route. You've done your company research

and

practiced answering the tough questions. You are perfectly prepared—and you still feel like a

nervous wreck.

You just got your paycheck. Your eyes scan down the list of deductions and

settle on the most important part—your take-home pay. You take that number and start

subtracting

your bills, your day-to-day purchases, or that expensive item you've got your eye on. However,

hiding in the often-overlooked payroll withholdings, you may find some untapped potential.

You just got your paycheck. Your eyes scan down the list of deductions and

settle on the most important part—your take-home pay. You start subtracting your bills, your

day-to-day purchases, or that expensive item you've got your eye on. However, hiding in the

often-overlooked payroll withholdings, you may find some untapped potential.

Making Money demonstrates that the ideal career path is a balance of skill,

income and passion. Students will learn to identify three types of income (wage, salary and

commission) and will have the opportunity to evaluate their dream job.

Making Money demonstrates that the ideal career path is a balance of

skill,

income and passion. Students will learn to identify three types of income (wage, salary and

commission) and will have the opportunity to evaluate their dream job.

Spending Money shows students how their spending choices can easily be

influenced by family, friends and popular culture. This content pack invites students to

consider

their own wants and needs. It also introduces the concept of opportunity cost.

Spending Money shows students how their spending choices can easily be

influenced by family, friends and popular culture. This content pack invites students to

consider

their own wants and needs. It also introduces the concept of opportunity cost.

Did you know that you get paid to deposit (or put) your money in a savings

account? Interest is the money a bank or credit union pays you for keeping your money in a savings

account. The longer you keep your money there, the more interest you earn. A savings account is

safer than a piggy bank and it makes you extra money, too!

Spending Money shows students how their spending choices can easily be

influenced by family, friends and popular culture. This content pack invites students to

consider

their own wants and needs. It also introduces the concept of opportunity cost.

For most people, spending comes

naturally. Saving up for something special

is harder. And setting money aside for

giving is really hard.

Spending Money shows students how their spending choices can easily be

influenced by family, friends and popular culture. This content pack invites students to

consider

their own wants and needs. It also introduces the concept of opportunity cost.

Writing a business plan is an essential part of building a successful business.

At its core, a business plan is a road map for your project: it establishes your purpose, it sets

goals and expectations, and it forecasts the relationship between cost and revenue. Business plans

exist in many forms: some formal and some informal.

Spending Money shows students how their spending choices can easily be

influenced by family, friends and popular culture. This content pack invites students to

consider

their own wants and needs. It also introduces the concept of opportunity cost.

Losing your job is stressful. Even with an emergency fund in place, it doesn't take very long to

feel the financial impact of a sudden loss of income. In order to reduce stress and stay

motivated, make sure that your income loss recovery plan

addresses the financial and non-financial aspects of losing your job.

The number of people working remotely is on the rise - and so are new trends in work-fromhome

fashion. For many, the ability to wear loungewear during work hours is a huge perk.

You may remember it as an equation you had to memorize for math class, but it's

so much more than that. It's the concept that powers all sorts of savings and investment products

and, over time, allows you to turn your money into, well, more money!

You may remember it as an equation you had to memorize for math class, but

it's so much more than that. It's the concept that powers all sorts of savings and investment

products and, over time, allows you to turn your money into, well, more money!

Every year, it's nice to do a bit of “financial spring cleaning” and

declutter

your filing cabinet, your desk drawers, and the various hiding places where miscellaneous scraps

of paper tend to accumulate and multiply. Read on to find out what you should be saving, and

what's OK to shred.

Every year, it's nice to do a bit of “financial spring cleaning” and

declutter

your filing cabinet, desk drawers, and the various hiding places where miscellaneous scraps of

paper tend to accumulate and multiply. Read on to find out what you should be saving, and what's

OK to shred.

Investing can seem like a very risky, complex and fast-moving process. With

endless combinations of investment vehicles to choose from, it can be difficult to take your first

step as an investor—especially with the knowledge that all investments carry the risk of losing

some or all of your money. So why bother?

Every year, it's nice to do a bit of “financial spring cleaning” and

declutter

your filing cabinet, desk drawers, and the various hiding places where miscellaneous scraps of

paper tend to accumulate and multiply. Read on to find out what you should be saving, and what's

OK to shred.

Traditional IRAs, Roth IRAs and 401(k)s

are all products designed to be an incentive

to save up for retirement. These accounts

act as containers for your investments.

Inside them, your money can grow and

accumulate tax-free.

Every year, it's nice to do a bit of “financial spring cleaning” and

declutter

your filing cabinet, desk drawers, and the various hiding places where miscellaneous scraps of

paper tend to accumulate and multiply. Read on to find out what you should be saving, and what's

OK to shred.

Bulls and bears can be considered the unofficial mascots of the stock market.

They represent the upward and downward movements of the stock market over a period of time and

have even come to describe investor behavior (optimistic investors are said to be bullish, while

investors with a pessimistic outlook are said to be bearish). In a field typically known for its

confusing financial terminology and often uninspired language, the bull and bear symbols really

stand out - and this is especially true in Lower Manhattan.

Every year, it's nice to do a bit of “financial spring cleaning” and

declutter

your filing cabinet, desk drawers, and the various hiding places where miscellaneous scraps of

paper tend to accumulate and multiply. Read on to find out what you should be saving, and what's

OK to shred.

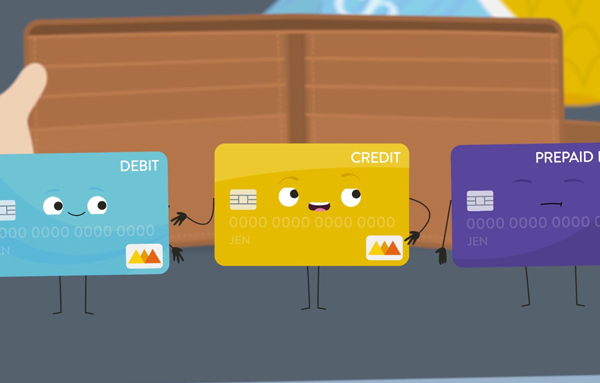

There are daily decisions that come into play for every bill you pay, every

tank of gas you buy,

and every coffee you pick up on the way to class or work. So, what difference does it really make

if you put your breakfast sandwich on credit instead of debit?

There are daily decisions that come into play for every bill you

pay, every tank of gas you buy,

and every coffee you pick up on the way to class or work. So, what difference does it really make

if you put your breakfast sandwich on credit instead of debit?

Credit card use plays a huge role in contributing to your credit history,

which

in turn is an

important part of your financial footprint. Credit scores are a key component in many of the

major

purchases you will make in your lifetime, such as vehicles or homes.

Credit card use plays a huge role in contributing to your credit history,

which in turn is an

important part of your financial footprint. Credit scores are a key component in many of the

major

purchases you will make in your lifetime, such as vehicles or homes.

Cómo usar tu tarjeta de crédito

Estos materiales están diseñados para fomentar una relación saludable entre los

miembros y sus tarjetas de crédito. Presenta los conceptos de ciclos de facturación, fechas límite

de pago y estados de cuenta de tarjetas de crédito, y aboga por “pagar el total y a tiempo”.

You've likely heard about credit scores before (thanks to all those

commercials

with terrible jingles), but what do you actually know about them? How long have they been

around?

And what's the deal with checking them?

You've likely heard about credit scores before (thanks to all those

commercials with terrible jingles), but what do you actually know about them? How long have they

been around? And what's the deal with checking them?

Desglose de una puntuación de crédito

Estos materiales te muestran cómo es que las puntuaciones de crédito se calculan y por qué son

importantes. Se te proporcionan consejos útiles para monitorear y mejorar tu puntuación de

crédito.

Credit scores are an area of personal finance that seem a lot more mysterious

than they actually are. Many people believe that improving them is a matter of trial and error

and, as a result, there's a lot of “credit score advice” floating around that can end up doing

more harm than good.

Credit scores are an area of personal finance that seem a lot more

mysterious

than they actually are. Many people believe that improving them is a matter of trial and error

and, as a result, there's a lot of “credit score advice” floating around that can end up doing

more harm than good.

Everyone has some idea of what it means to be money smart—however, whether

you've acted on that idea is a different story! There are a few nuggets of financial wisdom in

particular that are echoed so many times in articles, blog posts and TV segments that they become

clichés, albeit practical ones. Curb your spending. Pay off your debt. Contribute to your savings

early and often. Compound interest is your friend. Start saving now and watch your money grow.

Everyone has some idea of what it means to be money smart—however, whether

you've acted on that idea is a different story! Curb your spending. Pay off your debt. Contribute

to your savings early and often. Compound interest is your friend. Start saving now and watch your

money grow.

If you use a cellphone or have an email account, you've almost certainly been

exposed to an attempt at mass marketing fraud. Common examples include being interrupted by an

annoying robocall just as you start eating lunch, or waking up to a suspicious message in your

email inbox that somehow slipped through the spam filter. Sometimes, the attempted fraud is kind

of funny —the wording is so strange or the premise is so ridiculous (“An exiled prince needs my

help transferring a million dollars? Really?”) that we're left wondering how anyone could possibly

fall for such an obvious money grab.

If you use a cellphone or have an email account, you've almost certainly been

exposed to an attempt at mass marketing fraud. Common examples include being interrupted by an

annoying robocall just as you start eating lunch, or sometimes, the attempted fraud is kind of

funny —(“An exiled prince needs my help transferring a million dollars? Really?”) that we're left

wondering how anyone could possibly fall for such an obvious money grab.

Identity theft is nothing new, and yet it still manages to cost its victims

billions of dollars (yes, that's billions with a “b”) globally each year—not to mention the time

and hassle involved in recovering a stolen identity.

Identity theft is nothing new, and yet it still manages to cost its victims

billions of dollars (yes, that's billions with a “b”) globally each year—not to mention the time

and hassle involved in recovering a stolen identity.

Insurance coverage can be tricky to shop for because it requires making

specific financial decisions about some hazy and unpredictable concepts. Although individual

insurance policies & coverage details can seem endlessly complex, the fundamentals of insurance

coverage & your attitude toward it can be simple. Understanding the expectations of your insurance

policy can make much of the confusion and second guessing disappear, so you can focus in on what

you truly need from your insurance provider.

Although individual insurance policies & coverage details can seem very

complex, the fundamentals of insurance coverage & your attitude toward it can be simple.

Understanding the expectations of your insurance policy can make much of the confusion and second

guessing disappear, so you can focus in on what you truly need from your insurance provider.

Paying yourself first is an effective savings strategy because it takes

willpower right out of the equation. Rather than struggling to increase your self-control, you

simply reduce your need to put it in action.

Paying yourself first is an effective savings strategy because it takes

willpower right out of the equation. Rather than struggling to increase your self-control, you

simply reduce your need to put it in action.

Have you ever caught yourself daydreaming about all of the amazing lifestyle

changes that await you just beyond your next pay raise? Have you ever fantasized about how to

spend a work bonus, only to have the money instantly disappear into your monthly spending? If this

sounds familiar, you might be prone to lifestyle creep.

Have you ever caught yourself daydreaming about all of the amazing lifestyle

changes that await you just beyond your next pay raise? Have you ever fantasized about how to

spend a work bonus, only to have the money instantly disappear into your monthly spending? If this

sounds familiar, you might be prone to lifestyle creep.

Simply put, inflation refers to the rate of change or increase in the average

prices of goods and services typically purchased by consumers. When the price level rises, every

dollar you have buys a smaller percentage of a good or a service.

Simply put, inflation refers to the rate of change or increase in the average

prices of goods and services typically purchased by consumers. When the price level rises, every

dollar you have buys a smaller percentage of a good or a service.

Responding to Financial Emergencies

in Times of Uncertainty

The COVID-19 pandemic is a sobering reminder that financial challenges come in

all shapes

and sizes. Some obstacles - such as job loss or income reduction - are immediate and obvious.

Others - such as fear or uncertainty about the future - are more subtle, but they can still

disrupt

our regular spending and saving patterns in a negative way.

Learning a new skill has many potential benefits. It can entertain you, it can save you money, it

can boost your self-confidence, and it can unlock new opportunities at school and at work.

A savings account is a great place to store

your money at first. It’s safe and it pays a

little interest. But it won’t make you rich!

Growing your money requires that you

move some of it into investments with a

higher rate of return.

As a young adult, you may have heard the phrase “investing in the stock market” many times, but

you may not be sure what it means. Investing in the stock market means buying stocks, which are

shares of ownership in a company. Stocks can be risky investments because their value can go up or

down quickly, depending on various factors, such as economic conditions, company performance and

investor sentiment. Therefore, investing in the stock market can be intimidating, especially if

you are risk-averse or have limited knowledge of the market.

Retirement planning

can be a complex

endeavor. As you

approach your

retirement years, it

becomes increasingly

important to organize

your financial affairs

effectively.

Estate planning is the process of organizing and managing the distribution of your assets and

property after your death. While it may not be a pleasant topic to think about, it’s essential for

ensuring your financial legacy is distributed according to your wishes.

An emergency fund is an essential part of your personal finances. Its

importance is stressed in almost every personal finance book and budgeting blog, and yet 26% of

Americans currently have no emergency fund in place. Of those who do have an emergency fund, up to

two-thirds do not have the often-recommended six months' worth of expenses saved up.

An emergency fund is an essential part of your personal finances, and yet 26%

of Americans currently have no emergency fund in place. Of those who do have an emergency fund, up

to two-thirds do not have the often-recommended six months' worth of expenses saved up.

Is debt weighing you down? Look at your monthly budget and make a debt

repayment plan. If you can, pay more than the monthly minimum to pay down your principal balance

quicker, and if you receive any financial windfalls, use them to pay off debt.